Business

THE FRENCH LEGAL ACCOUNTING & TAX ISSUES RELATED TO ACQUIRE A US SUBSIDIARY

FRENCH AMERICAN PRIVILEGES

Escal Consulting Logo (Source: ORBISS/ Escal Consulting)

logo Orbiss

(Source: ORBISS/ Escal Consulting)

(Source: ORBISS/ Escal Consulting)

Marc Trost CEO of Orbiss

Source: Orbiss/ Escal Consulting

Source: Orbiss/ Escal Consulting

Logo Country wide Accounting Compliance

Source: IRC

Source: IRC

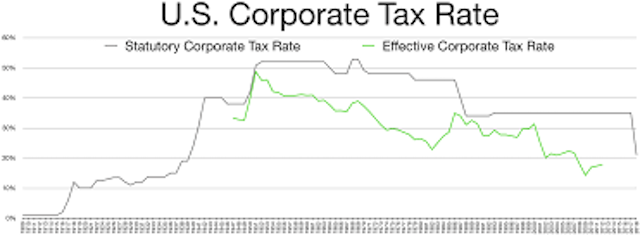

US Corporate Tax

Source: US Corporate Tax

Source: US Corporate Tax

Marc Trost Orbiss Tax Legal Accounting French American Subsidiary Procedures Rahma Sophia Rachdi Jedi Foster

Liability for this article lies with the author, who also holds the copyright. Editorial content from USPA may be quoted on other websites as long as the quote comprises no more than 5% of the entire text, is marked as such and the source is named (via hyperlink).